Africa Travel Week · 2026 Report

Unfiltered.

The 2026 State of African Tourism. For the last decade, African tourism sold a dream. Now, the market is demanding the receipt.

Trust Is the New Currency of African Tourism

For a decade, African tourism sold a dream.

For the last decade, African tourism sold a dream. In 2026, the market is demanding the receipt.

The post-pandemic rebound is over. The "Revenge Travel" wave has crashed. What remains is a more informed, discerning, data-driven traveller. They don't just want to see Africa; they want to trust it.

Trust used to be built on glossy brochures and bucket-list sunsets. Today, trust is built by algorithms deciding whether you exist, visa policies determining whether visitors can arrive, and EU compliance officers asking for your carbon audit. The tourism economy has become a verification economy, and many operators are still adapting to the new rules.

Here's what changed:

The numbers look good on the surface. Africa welcomed 81 million visitors in 2025 — 8% growth, the fastest in the world. In the first 10 months of 2026, for which data is available, OAG statistics show that there are 182.4 million departure seats available in Africa, a 13.7% increase on the 160.4 million available in the same period in 2025. Morocco is targeting 30 million visitors by 2030. Tanzania beat its 5 million target. South Africa hit 10.5 million arrivals.

But dig deeper and the picture fractures:

- Central and Western Africa recorded 0% aviation growth. Flat. While Eastern Africa exploded at +24.3%, an entire region was left behind.

- 72% of Gen Z use AI for inspiration for their trips, but if your lodge isn't API-ready, you're invisible to the algorithm.

- Less than 5% of Southern and East African properties hold third-party sustainability certifications, according to industry experts, yet from September 2026, the EU bans unverified "eco" claims. The greenwashers are about to face a legal reckoning.

The old playbook — build it, market it, wait for them to come — is dead.

This report argues that the new currency of African tourism is proof. Specifically, African tourism competitiveness now depends on five proof points:

The Five Proofs

-

1

Proof of Access — Airlift, visas, and ground connectivity

-

2

Proof of Discoverability — Digital infrastructure and machine-readable inventory

-

3

Proof of Credibility — Reviews, transparent communication, and service consistency

-

4

Proof of Responsibility — Sustainability evidence and compliance

-

5

Proof of Welcome — Operational inclusion and human readiness

The markets that are winning have aligned three things: policy, infrastructure, and data. Ethiopia's 31.2% aviation growth was deliberate investment in fleet and airports during the pandemic while others hesitated. Morocco's $13.6 billion in tourism revenue was visa liberalisation, seat capacity, and a trilateral World Cup strategy that turns a one-month event into a decade-long Mediterranean corridor.

The operators who are winning have stopped "doing luxury" and started "managing trust." In 2026, a US$10,000 safari is as much a trust transaction as a product. Guests are buying the confidence that the lodge actually supports the community, that the guide is trained, that the carbon offset is real, and that their same-sex relationship won't be a problem at check-in.

This report won't tell you that "Africa's time has come." The future is conditional.

It depends on whether:

- →

Tourism boards stop chasing volume and start building verifiable value

- →

Operators accept that inclusion is a $600 billion market test, not a nice-to-have

- →

Governments understand that policy chaos levies a "Trust Tax" on every business

The structure of this report reflects the new reality:

- 1

Part 1: The New Rules of Competitiveness. Dissecting the aviation map, the psychology of post-pandemic travellers, how Big Tech has changed distribution, and the incoming regulatory reckoning.

- 2

Part 2: The Welcome Test. Examining what "authenticity" actually means, and why inclusion is a commercial audit tested by LGBTQ+ guests, wheelchair users, and neurodivergent families who can smell performative marketing from a mile away.

- 3

Part 3: Where Growth Will Come From. Exploring sports tourism's undervalued "Sweat Economy," adventure tourism's economic multiplier, medical tourism's evolution from surgery safaris to burnout breaks, and wine tourism's reinvention as a full-scale lifestyle offering.

- 4

Part 4: What It Takes to Win. The infrastructure, capital, and workforce capability that will determine whether Africa captures the next wave or watches it land elsewhere.

The bottom line:

Africa has 81 million reasons to be optimistic and a dozen structural reasons to stay sharp. The dream is intact, but the market no longer buys dreams on credit.

In 2026, you either own the story with infrastructure, data, and truth, or someone else tells it for you, and you pay them commission for the privilege.

Part One

The New Rules of Competitiveness

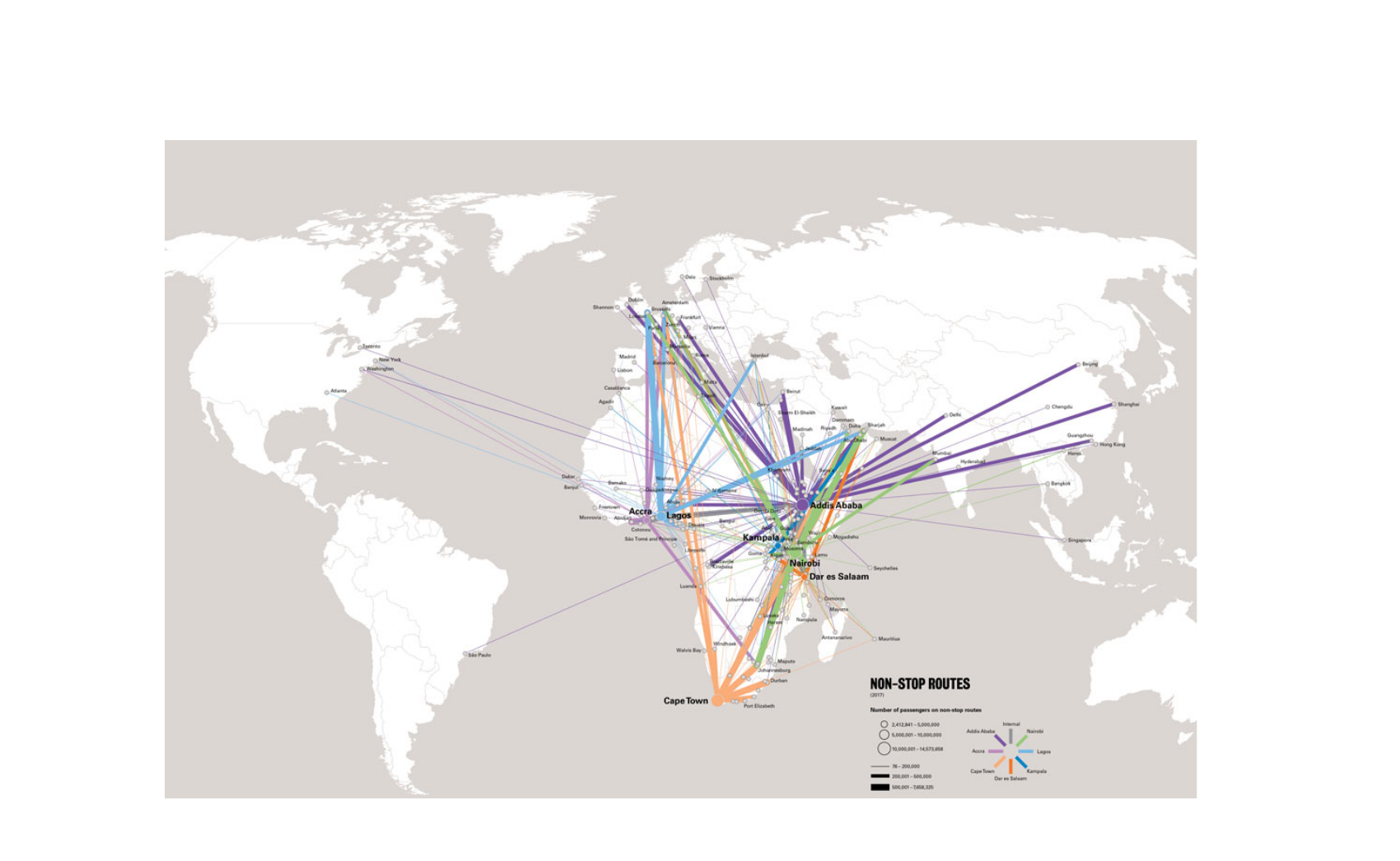

Proof of Access

Where Africa Stands

81M visitors · +8% · 182.4M departure seats

Eastern Africa surged +24.3% while Central and Western Africa stalled at 0%. Aviation capacity is not evenly distributed — and neither is growth.

Proof of Trust

Selling Certainty in an Anxious World

72% of Gen Z use AI for travel planning

The Trust Economy doesn't reward the most beautiful product. It rewards the most believable one. Credibility is now a commercial asset, not a soft skill.

Proof of Discoverability

The OTA Lock-In & AI Gatekeeping

Google UCP · Expedia Comet · API or die

If AI can't find you, you don't exist. The platforms have changed the game — and operators who aren't structuring their data for machine consumption are ceding ground they may never recover.

Proof of Responsibility

EU Green Transition Directive — Sept 2026

Only 4.3% of African properties certified

The EU's greenwashing ban goes live in September 2026. With 95.7% of Africa's hospitality inventory uncertified, this is not a future risk — it is a current booking barrier.

Where Africa Stands

Proof of Access

Snapshot

- Africa welcomed 81 million visitors in 2025 (+8%), but aviation growth is fiercely unequal.

- Eastern Africa is surging (+24.3%), while Central and Western Africa are flat (0% growth).

- The Bottom Line: Access is the new product. If you cannot be reached in one connection, you are a "someday" destination, not a "booking today."

Africa is the world's fastest-growing tourism region. In 2025, the continent welcomed 81 million visitors, an 8% increase that outpaced every other region globally.

But the real story is in the air. Aviation capacity surged by 13.7% to 182.4 million departure seats in the first 10 months of 2026, double the previous year's growth rate.

Aviation Heat Map — Departure Seat Capacity by Region (Jan–Oct 2026)

Source: ATTA Africa in the Air (March 2026)

What's Working

Infrastructure Investment Paying Off. Countries that built airports and expanded fleets during 2020–2024 are now reaping the rewards:

- Ethiopia: 31.2% seat growth — the fastest of Africa's top 5 markets

- Angola: New 15M-capacity airport driving 30% increase in arrivals ($667M revenue in 2025)

- Morocco: 22.5M seats (+21.8%) matching 19.8M arrivals and $13.6B revenue

Top Aviation Markets — Seat Growth 2026

Visa Liberalisation Accelerating Growth. 28% of intra-African routes are now visa-free, and the leaders are seeing results:

- Rwanda: Visa-free for all Africans | Source

- Kenya: ETA-free for African/Caribbean visitors (2 months) | BBC

- South Africa: ETA + MEETS for China/India, visa-free for Ghana, Kenya, Saudi Arabia, UAE, 6 European countries | Wikipedia

- Zambia: 50+ country visa-waiver (UK, USA) | Lusaka Times

Two Distinct Models Are Emerging

Connectivity Superpowers

Egypt, Morocco, South Africa, Ethiopia — building capacity to move millions through volume.

Experience Specialists

Tanzania, Botswana, Rwanda — restricting volume to protect yield. 2 million tourists spending $5,000 each vs. 20 million spending $500.

What's Not Working

Aviation capacity in Central & Western Africa is flat at 29.2M seats — no growth. Without infrastructure investment, this region risks being left behind while Eastern and Southern Africa surge ahead.

Tunisia saw a 50,000-seat reduction in 2026 after altering its aviation liberalisation approach — a reminder that policy shifts can have immediate impacts on capacity.

Aviation growth is outpacing ground connectivity. The Single African Air Transport Market (SAATM) has potential, but implementation remains patchy.

Localised conflicts in Sudan and the Sahel continue to affect continental image, despite their limited geographic scope — a perception problem that requires active counter-narrative work.

Access is the new product. If you cannot be reached in one connection, you are a "someday" destination — not a "booking today."

Selling Certainty in an Anxious World

Proof of Trust

Snapshot

- A traveller chooses Bali over your Zambian lodge. Not on price. Not on product. On trust.

- 72% of Gen Z use AI for travel planning — highest of any generation.

- The Bottom Line: The Trust Economy doesn't reward the most beautiful product. It rewards the most believable one.

Gen Z Travel Behaviour — 2026

A traveller is standing in their kitchen at midnight. Laptop open. Two tabs: a Bali villa they've seen on Instagram forty times, and the beautiful website of your lodge in Zambia. They close the laptop and book Bali.

You lost them. Not on price. Not on product. On trust.

This is 2026's defining commercial reality. Post-pandemic travel is driven by the need to feel certain in an uncertain world. And certainty, it turns out, is a commercial asset. Operators who can prove it win the booking. Welcome to the Trust Economy. You either have currency or you don't.

The Trust Equation

For Africa, Credibility is tanked by Western media. Self-Orientation is pushed high by "glossy" marketing. The only variable you fully control is Intimacy. This is your lever.

You're Not Selling Luxury. You're Selling Anxiety Management.

A Deloitte 2026 Outlook reveals a "bifurcated" market. High-income travellers are still spending, but have become hyper-cautious "deal-seekers," shortening trips to minimise risk. Meanwhile, the mass market is paralysed by economic fog. The middle ground is dead.

The Market Barbell — The Dead Middle

End 1: Commoditised Trust (The Safe Bet) — This is a Hilton in London or a Marriott in Dubai. The traveller trusts the brand. They know exactly what the sheets feel like. It is low-risk, transactional, and efficient.

End 2: Earned Trust (The Deep Dive) — This is the owner-run lodge in Zambia. The traveller trusts the people. They feel a personal connection, they participate in the conservation work, and they know the guide's name. It is high-risk but high-reward.

The Dead Middle — This is the generic, 4-star independent hotel that offers neither the safety net of a global brand nor the deep intimacy of a boutique lodge. In an era of high anxiety, this "middle" feels risky (no brand guarantee) and cold (no personal connection). If you are in the middle, you are invisible.

Hard Numbers

- 72% of Gen Z are confident using AI for travel planning — highest of any generation. (Skyscanner Trends 2026)

- 24% of travellers willing to pay more for volunteer opportunities; 15% for eco-tourism. (Euromonitor)

- 65% of travellers won't book a property without reading reviews first. Most read 6–12 reviews before deciding.

- 75% of Gen Z's destination choices are driven by social media. TikTok and Instagram function as their primary search engines.

- +8% Africa outperformed the global average (+4%) in 2025, reaching 81 million visitors. (UN Tourism / ATTA)

- 38% of Gen Z overspend chasing Instagram perfection, fuelling the "dysmorphia" trap. (PhotoAiD 2026 Social Media Travel Stats)

Four Trends Changing Who Books and Why

For decades, travel trends were about where people went. Croatia was in. The Caribbean was out. In 2026, geography is secondary. The new trends are defined by how people feel. Whether it's Gen Z fighting algorithmic anxiety or Boomers funding legacy trips, the following four trends have one thing in common: they're all about psychology, not postcards.

Travel Dysmorphia

Gen Z isn't just broke — they're stressed.

53% are open to "Role-Play Retreats." 69% would travel with a new friend specifically to test how they click. They want dirt, animals, and truth — not filters.

The Africa Angle: Sell the escape from reality — the "Readaway." Book a trip specifically to read books in quiet luxury.

Agentic Commerce

The Death of Search

In 2026, people don't search for travel. They instruct their AI and wait for results. 25–33% of travellers are already using AI tools for planning — a figure that tripled year-on-year.

"Travel isn't about where people go, it's about who they are." — Ben Harrell, Booking.com.

Participatory Luxury

"Viewing" is passive. "Doing" is trusting.

24% of travellers will pay a premium for volunteer opportunities. Don't sell a game drive — sell a conservation collaring operation. When a guest participates, they stop being a consumer and start being a partner.

"Gen Z factors sustainability into every booking — it's non-negotiable." — Kate Ferrara, Deloitte VP Hospitality

From Revenge to Reset

The hangover has cleared.

For three years, travel was fuelled by defiance. Now 67% of travellers say they no longer need a milestone reason to book; they just "deserve it." The motivation has shifted from "making up for lost time" to "protecting what's left of my sanity."

That's a different customer, with a different brief. Sell accordingly.

Trend 1: The "Travel Dysmorphia" Crisis

Gen Z isn't just broke; they are stressed. Research commissioned by Scenic Group reveals a generation suffering from "Travel Dysmorphia", the anxiety that their real lives don't match the algorithmic perfection of their feeds.

They don't want perfect sunsets; they want permission to be weird. This is why 53% of travellers are now open to "Role-Play Retreats" (fandom/cosplay tourism) and "Hushed Hobbies" (niche interests they don't share online).

Holidays in 2026 have become the ultimate compatibility check. Booking.com reveals that 69% of travellers are open to taking a trip with a potential partner or new friend specifically to see "how well they click." Nearly two-thirds (62%) would consider a remote location to test how their companion handles ambiguity. They also crave silence. 43% would travel specifically to feel closer to the natural world, not to photograph it, but to sit inside it.

The Africa Angle

Stop selling the "Big 5." Sell the escape from reality. Sell the "Readaway", a top trend identified by Expedia where travellers book trips specifically to read books in quiet luxury, disconnected from the noise.

Gen Z wants to disconnect from the dysmorphia and reconnect with a tangible reality they can touch. This drive for "grounded" reality is why Vrbo reports that searches for Farm Stays have surged 300% YoY. They want dirt, animals, and truth instead of filters.

Trend 2: Agentic Commerce (The Death of Search)

In 2026, people don't search for travel. They instruct their AI and wait for results. 72% of Gen Z are confident using AI to plan their trips — the highest of any generation. If your lodge's inventory isn't API-ready for an AI agent to read, you are invisible. Trust today means "digital reliability." Phocuswright notes that 25–33% of travellers are already using AI tools for planning, a figure that has tripled year-on-year.

Ben Harrell (MD US, Booking.com) sums it up: "Travel isn't about where people go, it's about who they are." If your product can't speak to identity, your AI agent won't surface it.

Trend 3: Participatory Luxury (The Antidote to Risk)

"Viewing" is passive. "Doing" is trusting. Euromonitor data shows 24% of travellers will pay a premium for volunteer opportunities. Why? Because participation builds intimacy — the numerator in the Trust Equation.

Don't sell a game drive. Sell a conservation collaring operation. Don't sell a village tour. Sell a skill-swap. When a guest participates, they stop being a consumer and start being a partner. That's when price stops mattering.

Trend 4: From Revenge to Reset

For three years after lockdown, travel was fuelled by defiance. People booked carelessly, expensively, urgently — making up for time stolen. That phase is over. The hangover has cleared.

Now, 67% of travellers say they no longer need a milestone reason to book a trip; they just "deserve it." They seek meaning over movement, prioritising mental health and "resetting" their nervous systems over ticking off sights. The motivation has shifted from "making up for lost time" to "protecting what's left of my sanity." That's a different customer, with a different brief. Sell accordingly.

The Trust Matrix: Generation by Generation

Generation by Generation

-

Gen Z

What They Crave: AI-assisted planning, "Dysmorphia-proof" authentic experiences

The Africa Opportunity: Live cams, conservation collabs, "Hushed Hobbies"

Stat: 72% confident using AI for plans (Skyscanner) · 53% open to role-play trips (Booking.com) -

Millennials

What They Crave: Multi-gen, sustainable flex

The Africa Opportunity: Kid safaris, BNPL bundles

Stat: 78% of millennials choose to spend money on a desirable experience over something material (World Economic Forum) -

Gen X

What They Crave: Value & reliability

The Africa Opportunity: Refundable rates, loyalty perks

Stat: 59% of Gen X prioritising exclusive rewards and discounts (Heuritech, 2025) -

Boomers

What They Crave: Premium intimacy

The Africa Opportunity: Private villas, human guides

Stat: 80% fund family trips (Booking.com)

Breaking the Echo Chamber

The Behavioural Economist — The Scarcity Mindset

Sendhil Mullainathan's, Professor of Behavioral Science, Chicago Booth/Harvard, research proves that "scarcity" (whether of money or time) physically shrinks a person's IQ. When the brain is preoccupied with economic stress, it loses "bandwidth."

The Travel Impact: A traveller with low bandwidth cannot process complex decisions. They default to "cognitive ease", booking the safest, simplest option (like an all-inclusive in Europe) rather than navigating the perceived complexity of an African safari. To win, Africa doesn't just need to be safe; it needs to be mentally effortless to book.

The Retail Sector — "Doom Spending"

Young consumers (Gen Z/Millennials) feel priced out of major milestones like buying a house. The result? "Doom Spending." Instead of saving for a deposit that feels impossible, they splurge on high-end skincare, luxury fashion, and travel.

The Travel Impact: Don't market your trip as a "savings goal." Market it as the immediate gratification they deserve in a chaotic world.

"The Trust Gap" — Edelman Trust Barometer

Trust in institutions (Government, Media) is at an all-time low. Trust in "My Peers" and "Technical Experts" is high.

The Travel Impact: A tourism board ad reaches fewer people than one honest review from a stranger who looks like your customer.

The Tax Nobody Sees (But Everyone Pays)

Trust is a tax. When a government creates policy chaos (visa blocks, sudden regulation changes), they levy a "Trust Tax" on every operator.

- The Evidence: Skift's Megatrends note that geopolitics erodes booking confidence 25% faster than economic downturns.

- The Lesson: South Africa's +11.8% inbound surge in Jan 2026 wasn't just about beaches; it was about the perceived stability following the election cycle. Stability lowers the "Risk" denominator in the Trust Equation, instantly boosting bookings.

THE TAKEAWAY: Build Your Trust Engine

- 1

Kill the Polish: Gen Z smells "fake" instantly. Use raw, user-generated content (UGC) to prove Credibility.

- 2

API or Die: Ensure your data is structured for AI agents to build Reliability.

- 3

Get Hands Dirty: Shift products from "observation" to "participation" to build Intimacy.

The Trust Economy doesn't reward the most beautiful product. It rewards the most believable one. Africa has the product. Now fix the proof.

The Game Is Rigged

How Big Tech Is Taking Over African Tourism

Snapshot

- 72% of Gen Z trust AI to plan trips, and platforms like Google and Expedia control the interface.

- Google's Universal Commerce Protocol (UCP) allows AI to complete bookings without the traveller ever visiting your website.

- The Bottom Line: If your inventory isn't API-ready, you are invisible to the algorithms that now control discovery. Data sovereignty is survival.

Platform Control of Booking Discovery — 2026

3 platforms control the interface · Google · Expedia · Booking.com

The "level playing field" is gone. Now, computers decide who gets the booking. You are not competing on ranking anymore. You are competing for inclusion.

Here's something you probably didn't know: the United Nations believes you have rights. Not just as a person, but as a tourism business. Rights to compete fairly. To reach travellers on equal terms. To benefit from the industry you help build, whether you're running a global hotel chain or a six-tent eco-camp in the bush.

In a new paper on artificial intelligence in tourism, UN Tourism introduced a concept the industry has long needed: a "level playing field." A digital world where everyone deserves a fair shot at being discovered, compared, and booked. The problem? That playing field is vanishing. UN Tourism is now sounding the alarm: AI is deepening inequality in the travel industry. Visibility — who gets seen, who gets booked — is increasingly decided not by the market, not by the traveller, but by algorithmic gatekeepers: Google. Booking.com. Expedia.

The Old Rules of Discovery are Changing

For decades, African tourism relied on relationships. Then came the internet. Suddenly, you needed SEO magic, direct booking websites, and OTA presence just to be found. Now comes the next shift — and it's happening faster than anyone expected.

When ChatGPT launched in late 2022, travellers started skipping the search engine altogether. No more opening 10 tabs and piecing together a trip. Now, they're asking AI to plan the entire itinerary. AI use in trip planning jumped 64% in just one year, according to Amadeus.

For African travel, the inaccuracies in AI-generated advice haven't been the biggest issue — yet. The continent's complexity still stumps many AI tools. But here's what's changed: AI is no longer just answering questions. AI works on top of existing booking systems — checking availability, filtering options, and directing travellers toward specific choices before they ever reach the actual booking platform. And that changes everything.

The New Gatekeepers: AI Assistants Decide Before Travellers Do

As hospitality analyst Brad Brewer put it in PhocusWire: "The OTA era taught us one painful lesson: whoever controls the interface controls the guest." In the age of AI, that interface isn't a website or an app. It's the assistant itself. And the companies building those assistants? The same ones already charging you commission.

The moment of decision — where to go, who to book — is happening inside platforms and ecosystems many African operators aren't part of. If your business isn't plugged into the systems feeding these AI assistants, you're not just getting outranked. You're getting erased before the conversation even starts. It's structural exclusion. And it didn't happen by accident. The infrastructure for all of this is live. And the biggest OTAs got there first.

Google's Universal Commerce Protocol

The latest shift is Google's Universal Commerce Protocol (UCP), which rolled out this year. Think of UCP as a change in the plumbing of how Google handles commerce. It's a master format — a common language — that lets all of Google's shopping, booking, and payment systems talk to each other seamlessly. Google built UCP for retail first (partnering with Shopify), but travel is next.

Before UCP, a traveller would search on Google, click through to a website or OTA, browse options, fill out forms, and complete a booking. With UCP, that entire journey collapses into a single conversation with an AI agent. A user asks Gemini a question — the AI searches inventory, confirms pricing, and completes the booking via Google Wallet — all without leaving the chat.

Here's the catch: you can't plug into UCP yourself. It only pulls from platforms and booking systems already integrated into Google's commerce infrastructure — and those are the major OTAs with the technical firepower and resources to build that connection. The playing field isn't levelling. It's narrowing.

To Be Visible in UCP, You Must Be:

- Listed on UCP-integrated platforms (major OTAs)

- Using booking systems with real-time API availability

- Feeding machine-readable data (pricing, descriptions, metadata) in the right format

When AI agents start handling bookings through UCP, you won't be an option — unless you pay to play. As Brewer warns, without intervention, hotels risk becoming "permanent renters in someone else's ecosystem." For African tourism, that's not just commission anymore. It's rent for the right to be discovered at all. The infrastructure was never neutral. And right now, the companies charging you commission are the same ones deciding whether you exist.

How OTAs Hijacked the AI Assistant

Three Ways OTAs Hijacked the AI Assistant

- 1. They got first dibs on discovery. Booking.com and Expedia were first to plug into ChatGPT's travel assistant tools — shaping itineraries from inside the chat. Travellers think they're getting neutral recommendations, but only OTA-listed properties show up. If you're not on them, you're invisible.

- 2. They built an "open" AI that only books them. Expedia teamed up with Perplexity to launch Comet — a sleek, downloadable AI that can do it all, including booking your honeymoon. But every travel search leads back to Expedia listings, turning a smart assistant into a one-brand booking trap.

- 3. They let viewers turn your reel into their sale. Expedia's "Trip Matching" lets someone watching your Instagram reel DM it with "Find me places like this." Their AI scans the scenery, but only recommends Expedia-listed stays — so your content sells someone else's room if you're not in the system.

Without intervention, hotels risk becoming "permanent renters in someone else's ecosystem." For African tourism, that's not just commission anymore. It's rent for the right to be discovered at all.

Brad Brewer, Hospitality Analyst, PhocusWireFour Actions African Tourism Must Take Now

-

1

Optimise for Generative Discovery (GSO, not just SEO) — Write descriptions AI can parse. Tag your Instagram with accurate locations. Use structured data wherever possible.

-

2

Claim Your Space on Dominant Platforms — Consider strategic presence on one or two major OTAs. Update your Google Business Profile. Make sure listing data is machine-readable.

-

3

Build the Direct Path Anyway — Get a real-time booking system. Capture direct contact info. Build loyalty loops. The OTAs want the transaction. You want the relationship.

-

4

Train Your Team to Be Smarter Than the Algorithm — Guests arrive briefed by bots that get Africa wrong. Use that. Communicate before they arrive. Be the human layer the machine can't replicate.

Loving It to Death

The Regulation of Experience

Snapshot

- Only 4.3% of Southern/East African properties hold third-party sustainability certifications.

- From September 2026, the EU bans unverified "eco" claims. Greenwashing becomes a legal liability, not just bad PR.

- The Bottom Line: Sustainability is now a B2B procurement requirement. If you cannot provide an audit-ready "data pack," you risk being dropped by European DMCs.

Certification Reality — Southern & Eastern Africa

⚠ EU greenwashing ban activates September 2026

The Double Crisis Nobody Wants to Talk About

Africa has two sustainability problems, and they are arriving at the same time.

The first is regulatory. From September 2026, the word "eco-friendly" becomes a legal liability under the EU's Empowering Consumers for the Green Transition Directive. Generic environmental claims will be treated as unfair commercial practice unless backed by hard, independently verified evidence.

The second is product. Africa is loving its wildlife to death. The same market forces that push "eco" into every brochure are also selling ever-closer encounters, ever-wilder content, and ever-fuller bed-nights — funnelling crowds into the same overstretched spaces and straining the very experience being sold.

One casual "eco" claim on a website with no independent verification behind it is now enough for a European buyer to look elsewhere. The risk is no longer worth it.

The Promise vs. The Reality

-

4.3%

The Promise: Safari brands market "low-impact luxury," "community upliftment," and "regeneration."

The Reality: Only 4.3% of properties in one major Southern/East African portfolio (roughly 60 out of 1,400) actually hold the third-party certifications to prove it. (JLL Research report) -

97%

The Promise: Guests feel good when they see local staff and a school visit on the itinerary.

The Reality: 97% of the market lacks the audited "data pack" now required to verify these impact stories for EU regulators. -

The Promise: Certification is marketed as a badge of honour.

The Reality: Staff at the source — even in iconic hubs like the Kruger and Cape Town — are often unable to define what their sustainability policy actually entails. -

The Promise: Marketing materials lean heavily on words like "green," "eco," and "responsible."

The Reality: These terms are a legal liability. Under the 2026 Directive, they are banned for EU consumers unless backed by recognised schemes. - <5% The estimated share of all African hotel properties with any form of accredited sustainability certification. (Global Sustainable Tourism Council)

- 20% of global consumers believe brands accurately represent their sustainability efforts. A further 26% outright distrust green claims. (YouGov)

- 600 Vehicles, 4,200 tourists — daily peak-season traffic at wildebeest migration viewing sites in Serengeti National Park. (Destination Stewardship Report)

- 53% of green claims examined by the European Commission were vague, misleading, or unfounded. 40% had no supporting evidence at all. From September 2026, this is outlawed.

- $195B Africa's estimated annual loss in natural capital, including illicit financial flows, illegal logging, mining, and unregulated fishing. (UNEP)

A Certification "Desert"

Liesel van Zyl, product manager at B-Corp certified Go2Africa, is already treating recognised standards as her reference point for a 1,400-property portfolio across Southern and East Africa. "From an operator point of view, when we want to be compliant, it's very difficult," she notes. While many partners perform well on the ground, only a fraction have the formal, third-party paperwork required to satisfy EU regulators.

To manage this, Go2Africa (under the Nawiri Group) launched a "Verified Sustainability" model in late 2025. By using their own Global Sustainable Tourism Council Criteria-aligned audit (or GSTC, the "Gold Standard" for sustainable travel) to bridge the gap, they can verify property impact immediately rather than waiting for formal certification. This ensures that the 97% of the market currently uncertified isn't simply abandoned, but is instead brought up to a verifiable standard.

At some of those properties… reservations consultants are asking, "What does sustainability mean?" And these are properties in the Kruger, Cape Town… in iconic areas.

Liesel van Zyl, Go2AfricaPaul de Waal, founder of the itinerary building platform Wetu, says the new rules mean every company has to collect sustainability information from all their suppliers. One large operator, he notes, hired staff just to send ESG questionnaires to about 1,000 suppliers. Six months later, only two-thirds had replied. Suppliers are fielding the same questions from dozens of partners, in dozens of formats.

His team built a standard self-assessment that properties complete once and share across the trade. "We're not measuring or asking for hard data," he says. "We're just asking to understand where on their sustainability journey they are." For him, schemes are "almost the accountants of sustainability": important, but not the point, which is to show the "good you do" — land care, staff welfare, community partnerships — to buyers.

The Lateral View: Brains, Law and Beds

Certification and audits tell buyers who to buy from, but they don't solve the underlying crisis: a market pushing operators to the breaking point. The same forces that push "eco" into every brochure also sell ever-closer encounters, ever-wilder content and ever-fuller bed-nights.

Environmental expert Dr Louise de Waal, director of the Blood Lions campaign to end commercial captive lion breeding and canned hunting industry, sees the consequences in parks and on social feeds. Travellers expect heightened access on a game drive or a weekend break, and guides and lodges are expected to deliver the impossible or risk the booking. With too many vehicles at a sighting, "animals start to become very comfortable and relaxed amongst vehicles and people," she says. That habituation looks good in photos, but "there's always an element of danger... accidents waiting to happen."

Marketing exacerbates the issue. When a regional airline, for example, runs an AI-generated image of a woman strolling next to a lion, the defence is that "it's not real", it normalises a fantasy of casual, intimate contact with predators. "Stop using AI to create videos of human wildlife interaction... because common sense is not common. And people ... want to do crazy things," De Waal says.

Cub petting is the most extreme expression of nature-on-demand. "People think they're supporting conservation, but it's pure entertainment," she says. Lion cubs are forcefully removed from their mothers shortly after birth, so they can be bottle-fed and handled. Once they outgrow the petting pen, many are channelled into captive hunts, breeding operations or the bone trade. "When people actually pet a cub, they take part in the killing."

What Guests Want

Melissa Foley, founder of All About Africa and a Travelife Sustainability Auditor, has been a leading voice warning the trade about the EU Directive, yet she sees the demand side with pragmatism. Her American clients care about the Big Five, the right dates and the right price. Sustainability "is not actually a marketing differentiator. It's not even a sales USP... it's something that we're doing because it's the right thing to do and it's because we want to."

The irony is guests only notice the impact work once they arrive. "Often I'll hear a guest saying, 'Wow, this is amazing that this lodge is supporting this community,' but they never asked about that leading up to it." The end-consumer is still chasing sightings and stories.

Overtourism and Carrying Capacity

The industry has trained guests to expect the "money shot" — the river crossing, the kill, the cheetah on the bonnet — squeezed into a game drive. When those moments don't materialise, tourists view the trip as a failure.

That puts pressure on guides. Tips and repeat business hinge on whether they can "deliver the crossing", which nudges behaviour towards aggressive off-roading, edging closer than is safe, or joining the "wall of steel" traffic jams. The viral Serengeti clip from 2025, where more than a hundred game drive vehicles stacked along the Mara River, guests out of cars, everyone jostling for the same crossing, was the expected outcome of selling nature as guaranteed drama.

"That Serengeti incident can happen really anywhere," says Van Zyl. Her team now trains consultants to sell low-impact safaris instead. "These provide a better experience for the client. It is also better for the environment."

Rwanda & Uganda: The Limit Is the USP

Each habituated gorilla family sees a maximum of eight trekkers for one hour a day. Fewer than 200 permits are issued daily, at prices of up to US$1,500 — and they still sell out. The experience is rationed, the product is protected, communities are funded, and the limit is the unique selling point.

Van Zyl is clear about where the industry is heading. "We haven't yet said to somebody, 'We are not going to use you anymore because you don't have impact,' but we do need to, at some point in the near future, start to then say, well look, if you're actually just not interested at all, then we cannot keep you."

Sustainability isn't a marketing differentiator or a sales USP for the guest — it's something we do because it's the right thing to do. The irony is they only notice the impact once they're on the ground.

Melissa Foley, All About AfricaWhat Leaders Need to Do Next

- →

Clean up your language immediately. Before September 2026, audit every piece of marketing for unverified environmental claims. This is legal hygiene, not optional.

- →

Use certification as a shortcut, not a burden. The cost of certification is lower than the cost of losing a European DMC relationship.

- →

Start where you are. Begin with local employment data, energy consumption figures, and invasive species records. Build from there.

- →

Design the limit as the product. The low-impact safari is not a compromise. It is a better experience.

Part Two

The Welcome Test

Authenticity — The Real Deal

Snapshot

- Farm stay searches up 300% YoY (Vrbo). 24% willing to pay more for cultural immersion (Euromonitor).

- The Bottom Line: Authenticity cannot be transferred or copied. The experiences that resonate most are designed with the people of a place, not for tourist expectations.

Demand Signals — 2026

Farm stay search growth year-on-year (Vrbo)

Willing to pay a premium for cultural immersion

"Authentic" has fast become travel's favourite adjective… with each new lodge, experience, and destination marketing campaign invoking the same promise. But is the word now doing so much work that it risks meaning nothing at all?

For Jacqui Taylor, founder of Agritourism Africa, authenticity is rooted in rural towns, farms and landscapes, where nature is restorative and people are simply who they are — without pretence or performance.

For Judy Kepher-Gona, founder and executive director at Sustainable Travel and Tourism Agenda (STTA), authenticity, rural or urban, is defined by the people of a place, unique to its context, and only real when a community can see its own values, identity and voice reflected in an experience.

Together, they begin to build a picture of what authenticity in travel should look like — for a generation of travellers who "are on a quest for highly personalised journeys."

This according to Hotel Link, whose 2026 insights (drawing on trend data from Booking.com, Expedia, Skift and Amadeus) reveal a new chapter for the tourism industry. One where:

- Visitors prioritise boutique hotels, creative stays or eco-lodges over mass-market hotels (Booking.com)

- Vrbo.com has seen a 300% year-over-year increase in guest reviews mentioning farm-related experiences (Expedia)

- Travellers look to "reset themselves" through nature, retreats and digital detoxes, with wellness tourism forecast to reach $8.5 trillion by 2027 (Global Wellness Institute)

Euromonitor's data shows a similar pattern with 24% of travellers willing to pay more for volunteer opportunities, 15% for eco-tourism, and 12% for local cultural immersion.

Ultimately, the experience economy is becoming more intentional. Think enrichment over entertainment, with visitors looking for experiences that are deeply grounding, authentic and purposeful.

The Guidebook Problem

But who gets to decide what's authentic? As Kepher-Gona explains, we're looking at it through different lenses. Is it the traveller who defines what is real? Is it the people of the place who define what is real? Or is it the tourism operators who package things and call them real?

Part of the problem lies not with the industry, but with the traveller. Many visitors arrive with a fixed, often decades-old idea of what a place 'should' look like — and are quietly disappointed when reality doesn't match it. Kepher-Gona has seen this pattern repeatedly across East Africa: visitors who have read guidebooks written thirty, forty, fifty years ago, who arrive expecting 'wild Africa' and are unsettled to find Maasai community members with smartphones and mobile banking.

They come to places and say, oh, but this is not authentic. People are wearing clothes. They have a watch like mine. But what they are expecting would just be performative. It wouldn't be real at all.

Judy Kepher-Gona, Sustainable Travel and Tourism AgendaWhat those travellers are seeking is not authenticity. It is a performance of the past. And the instinct to provide it — to dress experiences in the costume of a culture that no longer exists in that form — sells both the traveller and the community short.

As Kepher-Gona puts it, culture and heritage should not be used to hold communities hostage. The Maasai lawyer who wears a suit to court also dresses in full traditional attire for a rite of passage. Both are real. Neither cancels the other.

Taylor agrees and adds a dimension that is too often missing from the conversation: education. Travellers arrive with assumptions, she argues, and authentic experiences have a responsibility to gently update them. Education is not an add-on to an authentic experience. In many cases, it is what makes the experience authentic in the first place.

Performance, Presentation, and the Real Thing

The travel industry has long conflated three very different things: a historical presentation, a curated performance, and genuine authenticity. They are not the same — and treating them as interchangeable is where credibility is lost.

Kepher-Gona is not opposed to a historical performance. A demonstration of how the San people of Namibia once lived can be a rich and meaningful experience. The problem arises when it is sold as something it is not. She recounts a traveller who visited a village in the Namibian desert, genuinely believing they were meeting an indigenous community living as their ancestors had. It was only later that a community member quietly admitted: "We don't live here. When guests come, we are invited. We change into these clothes and get our traditional things."

The solution, Kepher-Gona argues, is simple honesty. "Say you will see a presentation of how they used to live. Don't say they are living their traditional lives." The experience itself loses nothing. The deception is removed.

The most compelling examples of genuine authenticity, both experts agree, share an unexpected quality: they were never designed around a tourist's expectation at all. In Mombasa, tuk-tuk drivers who have navigated every corner of the city for decades, acting as unofficial guides for food, nightlife and shopping. Or an operator forging a relationship with a local fisherman — leading to sunrise excursions and foodie experiences as his wife cooks the catch. In Gabon, a community homestay project that offers visitors direct engagement with rural life, ensuring that economic benefits stay within the community. In Ethiopia, rural coffee tours that take you into the Kafa Biosphere Reserve, one of the few remaining wild coffee forests in the world. In Zambia, a convent stay with nuns from around the world, giving a peaceful, authentic stay unlike anywhere else.

Demand Is Real

This is not an abstract conversation. The market is moving, and the evidence is vivid.

Recently, an American influencer documented a ride on one of Nairobi's iconic, art-covered matatu minibuses — playing music, painted floor to ceiling, a moving theatre of urban Kenyan culture — and the response was global. Within months, Germany's Deputy Chancellor was sitting in a matatu, eating street food, being driven through every corner of Nairobi on a six-hour city tour.

"Authenticity creates demand," says Kepher-Gona. "When it's really authentic, people want it."

Taylor sees the same pull in agritourism, which exploded globally after COVID as travellers sought not only to understand themselves — but also the ancient rhythms of life, how land is worked, and what rural life actually looks like. She is currently working with communities across Southern and East Africa where the appetite is real and growing — including two new businesses that approached her in the same week, both built entirely around the idea of helping people reconnect with who they authentically are.

How to Build an Authentic Experience

What separates a genuinely authentic experience from a performative one? Between them, Kepher-Gona and Taylor have worked across dozens of destinations, communities and tourism contexts. Their collective answer has nothing to do with aesthetics, production value or marketing spend.

Authentic experiences can be built — but only with the right intentions, and only by the right people. As Kepher-Gona puts it, authenticity can be restored even where it has been lost. "We can restore it where it is lost," she says, "but only by being intentional."

The industry already has the tools. What it requires is the honesty to use them properly — and the humility to let the people of place lead the way.

Lessons from Agritourism

For Taylor, the non-negotiables for agritourism are sustainability, community engagement, quality and authenticity, collaboration and innovation and diversification.

Agritourism Policy Principles

Six Principles from Those Who Know

- 1

Start with the community, not the concept. Authentic experiences are designed with the people of a place, not for them. Consultation is not a checkbox — it is a solid foundation.

- 2

Be honest about what you are offering. A presentation of how people used to live can be just as powerful as witnessing how they live today. The problem is not the performance; it's the mislabelling.

- 3

Let the place be the differentiator. Authentic is not transferable. The experiences that resonate most are the ones that could only exist here, on this land, with these people.

- 4

Bring education into the encounter. Travellers arrive with assumptions. Authentic experiences gently update them — helping visitors understand a vibrant, living, evolving culture.

- 5

Invest in the people of the place. The tuk-tuk driver who knows every corner of Mombasa. The fisherman whose wife cooks the catch.

- 6

Lead with intention. As Taylor says, "If someone can explain to me what the intention is, then everything becomes clear. Otherwise, it's quite a murky environment."

The Small Towns, Authentic People and Great Stories — Waiting for You

Travel blogger and freelance travel writer, Bob Bales, sums it up beautifully: In 2026, it's not just where people want to go, but how they want to travel, why they want to travel, and what they are quietly trying to escape.

Small towns are surging — just ask industry legend and founder, Ron Mackenzie, whose Facebook group Small Town South Africa boasts well over 270,000 members (and growing by the day). People are looking for somewhere with a sense of story, a sense of place, and a slower pace.

For Taylor and Kepher-Gona, authentic travel, at its best, offers all three. You just have to look for it.

The Inclusion Promises We Can't Keep

Snapshot

- The LGBTQ+, reduced mobility, and neurodivergent markets are $600 billion economic blocs.

- Performative marketing — rainbow logos, token ramps — is commercially and ethically insufficient.

- The Bottom Line: Inclusion is not a values exercise. It is a commercial audit. And it's being tested right now.

The Inclusion Market

Combined LGBTQ+, reduced mobility & neurodivergent travel markets

of global population lives with some form of disability

If authenticity is the promise, inclusion is the audit. You cannot claim to offer 'radical African hospitality' if your welcome is conditional.

The global tourism industry loves the slogan 'all are welcome'. It looks good on websites and plays well in sales decks, but it doesn't always ring true. Particularly here in Africa, the lived reality too often contradicts the marketing:

- Luxury lodges actively courting the high-spending LGBTQ+ traveller in countries where their lifestyle is criminalised.

- Hotels claiming 'accessibility' because they installed a single ramp (that ends at a step).

- A near-total blind spot when it comes to neurodiverse travellers, with approximately 15–20% of the global population within the neurodiversity spectrum.

Why does this matter?

Inclusion claims are being tested by buyers and travellers. When promises don't match reality, the consequences are immediate: lost business, reputational damage, and legal risk. Getting it wrong is costly. Getting it right is a competitive advantage.

It's time to zoom out and assess the bigger picture. Where are opportunities being missed by overlooking travellers once labelled 'niche', but are firmly embedded in the mainstream tourism economy?

Right now, the industry needs every pathway to success. When one business wins, the ripple effect lifts us all as a community. Tourism doesn't operate in isolation; it fuels multiple adjacent sectors, and together this ecosystem underpins the broader economic health of African nations.

1. LGBTQ+ — Not Just Pink and Rainbows

Contributors: Jason Fiddler, Founder and CEO of Pinq Travel & LoAnn Halden, VP Communications, IGLTA

The market now: LGBTQ+ travellers represent a powerful economic force, with global spending projected to reach nearly $600 billion by 2030. As Fiddler notes, if global LGBTQ+ spending were a country, it would rank among the world's largest economies.

Who are they? As Fiddler emphasises: "LGBTQ+ tourists are not all wealthy, white and Western. They hark from all walks of life." They tend to be extremely wanderlust and determined travellers, often taking financial risks to finance trips abroad or locally. Halden encourages Africa's tourism industry to remember: "We are individuals, not dollar signs… our individuality is a reflection of what it means to be human, and humans bring value when they are valued."

What do they need? At its core, the requirement is simple: inclusion. "Inclusion comes with respect," adds Fiddler, "and respect creates a comfortable traveller experience." They seek destinations that are safe and welcoming, but also culturally rich and authentic.

Legal tension: In more than 30 African countries, LGBTQ+ identities remain criminalised. As Halden notes, "Some of the most targeted legislation against our global community has come from African countries, and unfortunately, that cloaks the entire continent in suspicion."

The rainbow-washing trap: Slapping a rainbow flag on a logo during Pride Month is easy. Training staff to treat same-sex couples with the same ease and respect as any other guests is the real work — and the part too often skipped. Travellers notice quickly when inclusion is performative. Avoiding that trap requires genuine engagement, awareness, and operational policies that prioritise safety, dignity, and respect.

The way forward: Drop the assumptions. Invest in consultation, education and continuous training. Engaging with those who truly know the market and can guide, inform, and help get it right. One must constantly understand what is happening in this market. "You can't be in tourism and make assumptions about your market," Fiddler warns. "Inclusion is not about politics or culture wars; it is about good business. Tourism is not a charity. It is a commercial industry, and inclusion is one of its strongest growth strategies when done with honesty and care." Halden urges operators to start locally: "Connect with your local LGBTQ+ community. Understand how tourism impacts them and ensure they have a genuine seat at the table." She recommends joining the International LGBTQ+ Travel Association and making use of its free resources: "Invest in training for your teams. It's the best money you'll ever spend!"

Additional resources: pinqtravel.org, iglta.org, kzngalta.org.za

2. Reduced Mobility & Access — More Than Just a Ramp

Contributor: Sherise Dreyer, Inclusive Marketing, Branding & Communication Strategist

The market now: Approximately 1.3 billion people, or 16% of the global population (1 in 6 people), have a significant disability — a number rising due to ageing populations. This segment is part of the mainstream tourism economy.

Who are they? Reduced mobility travellers do not represent isolated transactions. While some travel independently and frequently, many travel with partners, children, families, colleagues, and networks.

What do they need? "From a humanised experience, it's no different to what you and I would want to experience," says Dreyer. "Sometimes it's just a perception shift. It's not moving barriers; it's how you interact and understand where their specific needs are."

The adventure gap: Can a wheelchair user go on safari? Some operators are innovating with adaptive vehicles, while others simply shrug and say, "Sorry, it's the bush." South Africa's adventure tourism industry generated R12bn in direct revenue in 2024, and adventure is a top interest for mobility-impaired travellers, according to Dreyer.

Performative accessibility: A 'compliant' room may technically have a rail, but a truly usable room considers everything: low mirrors, manageable carpets, and staff trained to assist. Ramps in the right place are useful, but without a humanised experience and perception shift, they're meaningless.

Filling in the data: Data gaps remain a barrier. Detailed insights into mobility travellers are limited, making it hard for operators to design remarkable experiences. But if you don't know the questions, how can you address the needs? Dreyer emphasises: "Seek them out, speak to them, engage, understand, then act."

The way forward: The industry doesn't need more symbolic gestures; it needs structural commitment. When inclusion becomes normal, economics follows. That means education and sensitisation across every role, from safari guides to hotel cleaners, embedded into strategy, KPIs and daily operations. As Dreyer puts it: "Stop portraying disabled people as the 'other'. Make accessibility the norm. Inclusion should be part of everyday strategy and normalised as standard practice — your way of living, your mindset, your KPIs, whatever you're doing in your marketing. This is not only about moving barriers or running campaigns; it's a human shift, a mindset shift. And it is entirely a choice."

Additional resources: disabilityinfosa.org.za, ncpd.org.za, bradshawleroux.co.za

3. Neurodiversity — The 'Invisible' Travellers

Contributor: Adrian Lange, father to an autistic daughter and CEO of Tourism that Cares

The market now: Neurodivergence includes a range of atypical developmental norms — autism, ADHD, dyslexia, and Tourette's among the most recognised. By 2026, the global shift has moved beyond awareness to inclusion in schools, workplaces, and increasingly, travel.

Who are they? More than 30% of adults globally are neurodivergent, with some estimates closer to 40%. One in five people worldwide identifies as neurodivergent, and over half of Gen Z do. This is not an invisible traveller. It is an underserved market.

Sensory reality: Tourism in Africa is intensely sensory: loud airports, bright lights, unpredictable transport, crowded markets. For autistic travellers or those with sensory processing differences, these environments can be overwhelming. Unlike destinations with established support systems, African travel requires careful planning and a hands-on approach to ensure journeys are not just possible, but comfortable.

Low cost, high impact: Quiet hours, sensory maps, 'what to expect guides', predictable check-in processes, and clear communication remove friction without major capital spend. Lange emphasises that staff neuroinclusion training courses are available.

The family market: Families with neurodivergent children are a large, loyal segment actively seeking safe, understanding destinations. When they find places that work, they return — and they recommend them.

The way forward: As Lange notes, "Sometimes it's just a perception shift. It's not moving barriers, it's how you interact with the traveller as a human being and understand where their specific needs are." Not every traveller will disclose their needs — that's where empathy and the confidence to ask "How can I help?" matter most. "Two people can see the same experience differently," Lange explains. "Inclusion is not about standardisation. It's about flexibility. Design for humanity first, and better tourism follows."

Additional resources: aut2know.co.za, tourismthatcares.com

Final Thoughts

Populations are ageing. Disability prevalence is rising. Neurodiversity awareness is expanding. At the same time, travellers are more value-driven and information-rich than ever before. Inclusion is no longer a niche concern or a moral add-on; it is a structural market shift that is reshaping global tourism.

Tourism, and how we present it, reflects our countries and who we are as societies. When we practise care at home, we are better equipped to care for visitors. When we learn to empathise with travellers who may seem different at first, we strengthen understanding and compassion within our own communities.

The impact is circular: inclusive tourism builds inclusive societies, which in turn support more authentic, resilient visitor experiences. Only then can we credibly stand behind the promise and work toward the reality of "All Are Welcome."

Part Three

The Growth Sectors

Sports Tourism

The Sweat Economy

The recurring school sports ecosystem and spectator tours fill multi-room bookings and drive high-yield shoulder season revenue — year after year, not just at the World Cup.

The Recovery Economy

From Surgery Safaris to Burnout Breaks

Corporate burnout is costing global economies billions. Africa is positioned to become the world's premium "nervous system reset" destination — and the B2B pitch writes itself.

The Modern Wine Traveller

USD 108B → USD 358B by 2035

Wine tourism is luxury tourism. The modern wine traveller drinks less but spends more — on trails, beds, and winemakers telling their story outside the cellar. The Cape Winelands Airport opens in 2028.

Adventure Tourism

The Economic Multiplier

R25 billion total economic impact. 91,000+ jobs. Africa's adventure market is projected at USD 53.9B (CAGR 11.2%). Thumbs are not meant for the space bar.

Sports Tourism — The Sweat Economy

Where Growth Will Come From

Snapshot

- Sports tourism is a $2.8 trillion global market by 2030, yet Africa consistently views it through the narrow lens of the mega-event.

- 92% of sports-interested South Africans want to travel locally. 78% have children under 18 — they are experience-hungry, multi-room bookers who use the sporting event as an anchor, not the entire itinerary.

- Chase the parents, not the podium. The real ROI in sports tourism is not the World Cup. It is the school hockey tournament that fills 130,000 hotel beds over Easter weekend, year after year.

The Revenue Model

School sports tours — annual, recurring, multi-room bookings, shoulder season revenue

FIFA World Cup — Morocco / Spain / Portugal. Once per generation.

Johannesburg and London are the only two cities in the world to have hosted a World Cup final for cricket, rugby, and football. Yet, despite this world-class pedigree, the sports and tourism sectors are still running parallel races instead of a unified relay.

The problem? Almost no one is treating sports fans like the high-yield, multi-room, shoulder-season opportunity they actually are. For too long, the tourism industry has viewed sports through the narrow lens of the marquee event — the once-in-a-decade mega-tournament that dominates planning cycles and marketing budgets. The reality is that sports tourism is a sleeper economic powerhouse with the rare ability to stabilise seasonality, fill beds in secondary towns, and distribute tourism revenue far beyond traditional leisure hubs.

Sports tourism is also a critical, yet often misunderstood, component of the MICE ecosystem. Athletes rarely travel alone. They bring coaches, medical teams, and families — and they stay longer.

"Then generally, they stay for longer. They want to acclimatise, so they'll arrive a few days before because they want to get used to the terrain. We're looking at longer lengths of stay when it comes to sports events. And then obviously supply and demand, the ADR goes up, the prices go up."

Lee-Anne Singer, Chairperson, FEDHASA Western CapeWhy Now? The Profile Nobody Expected

Nielsen Sports South Africa's 2025 Fan Insights survey reveals a sports tourism market that is younger, more diverse, and more domestically focused than the industry assumes.

Who Actually Travels for Sports?

- 55%Female — challenging the assumption that sports tourism is male-dominated

- 78%Have children under 18 — making them multi-room, multi-night bookers

- 78%Are Black — underscoring the growth of the domestic African middle-class market

- 63%Earn between R5,000–R39,999/month — solidly middle-income, but willing to spend on experiences

- 92–93%Show strong interest in domestic travel — the highest intent of any leisure segment

These are not one-dimensional "sports fans." They are experience-hungry travellers who use the sporting event as the anchor, not the entire itinerary. They want food festivals, live music, adventure activities, and cultural events alongside the match. The Durban July is not just horse racing; it is fashion, food, and social currency. If operators market only the match and ignore the wine farm, the mountain bike trail, or the township food tour, they are leaving the majority of the wallet on the table.

The Mega-Event Question: Spike or Shift?

South Africa 2010 proved that Africa could host the world. Morocco 2030 is attempting to prove that hosting the world can fundamentally modernise a nation's economy. The shift is from the "one-month spectacle" to a "borderless Mediterranean corridor" — and for African tourism operators, that distinction matters enormously.

SA 2010 vs. Morocco 2030

- $3.6BSA 2010 direct economic impact. Gautrain, stadiums, airports as infrastructure legacy. A national showcase.

- $40BMorocco 2030 estimated investment budget. Al Boraq high-speed rail expansion, multi-purpose venues, digital infrastructure. Target: 30 million annual visitors via trilateral corridor with Spain and Portugal. A decade-long Mediterranean tourism corridor.

As Kelvin Watt, Chairperson, Nielsen Sports South Africa, points out, single-sport events like the World Cup are inherently less financially risky than the Olympics because they can leverage existing infrastructure. South Africa's stadiums remain vibrant assets 15 years later.

The Real Sweat Economy: School Sports and Spectator Tours

Tier 1 — School Sports (Highest Frequency, Highest Cumulative Yield)

The school sports ecosystem is a multi-billion rand industry that is currently undervalued and largely unpacked by major tourism stakeholders. When a child travels for a tournament, they don't travel alone. They bring an entire support squad — parents, siblings, coaches — leading to multi-room bookings and extended stays in towns that leisure tourism rarely reaches.

"Athletes for these kinds of events tend not to visit restaurants and pubs and participate in things other than the event. They'll go there, they'll eat minimalistically... they'll drink a lot of water, they'll participate and they'll typically leave."

Kelvin Watt, Chairperson, Nielsen Sports South AfricaThis observation is critical: the real spend is not the athlete. It is the family. It is the parent who books the restaurant, the sibling who buys the experience, and the coach who extends the stay for a game drive.

The Scale of School Sports Tourism

- 130,000People flow into Johannesburg over a single Easter weekend, driven by just 22,000–26,000 school athletes and their families

- 450School hockey teams travelled to South Africa in 2024, primarily from the UK, Chile, Argentina, Australia, and New Zealand

- 150+British private schools regularly send mega-tours of 150+ children, with full contingents of staff, parents, and siblings across rugby, netball, and hockey

- Top-tier rugby schools from Australia and New Zealand, including St Joseph's Nudgee College and Westlake Boys High School, participate in prestigious South African festivals like the St. John's College Easter Rugby Festival.

- Zimbabwe and Namibia are significant players in this circuit, creating a resilient regional travel economy built on annual, recurring school festivals.

These tours represent a high-frequency, plannable revenue source — often recurring annual events that allow tourism operators to forecast and prepare years in advance. Something no mega-event can offer.

Tier 2 — High-Value Spectator Tours (Moderate Frequency, High Yield)

Professional spectator tours — such as the upcoming Greatest Rivalry Rugby Tour when the All Blacks tour South Africa — bring fans who stay for weeks, hitting wine farms, restaurants, golf courses, adventure activities, and safaris between matches. Unlike mass participation athletes, these visitors spend broadly across the tourism ecosystem.

Tier 3 — Mega-Events (Low Frequency, High Visibility)

Mega-events like the Comrades Marathon and Cape Town Cycle Tour are iconic but must be understood for what they are: high-visibility, low-dispersal events. Mass participation athletes spend minimally outside their event. The real value lies in the media exposure and destination branding they generate, not the per-head spend.

The Data Blind Spot

The industry's greatest structural hurdle is not a lack of talent or facilities. It is a chronic lack of hard data. While airport arrivals can be tracked with 100% accuracy, the actual economic footprint of a sports tourist once they leave the terminal remains largely anecdotal. Hotel reporting is voluntary, and many smaller operators do not report data. Subscriptions to tracking services like STR/CoStar are unaffordable for many operators.

This transparency gap prevents the sector from lobbying Treasury (without data, it is nearly impossible to motivate for better funding), countering over-tourism narratives, and deploying marketing spend effectively.

Hard Stats

- 1:2.5For every one sports visitor, an estimated 2.5 employees in the tourism industry are supported

- R600M+Annual economic contribution of the Comrades Marathon to the KwaZulu-Natal economy, supporting approximately 1,800 jobs

- $2.8TProjected global value of sports tourism by 2030, with an implied annual growth rate of roughly 17.5%

Why It Matters Commercially: From Athletes to Property Owners

The impact of sports tourism extends into unexpected long-term territory. High-profile international players (such as those in the SA20) have begun buying holiday homes in areas like Paarl and Val de Vie after spending tournament time there. The 2010 FIFA World Cup delivered long-term earning assets — the Gautrain, upgraded stadiums, and expanded airports — that continue to facilitate all forms of tourism today.

In Mossel Bay, the municipality shifted from operating assets to enabling them, leasing campsites to private operators. This turned underutilised assets into steady income streams while filling the town with thousands of visitors for recurring events like the Ironman. It is a replicable model.

What Leaders Must Do Next

- 1

Chase the Family, Not the Athlete. Package the purpose of travel. If 450 hockey teams are visiting, proactively market safari bundles, local dining, and adventure activities to their families months in advance. The athlete's spend is limited. The family's spend is not.

- 2

Build the Data Infrastructure. The sector cannot lobby, market, or plan without data. Operators must collectively push for standardised, voluntary reporting mechanisms that allow the industry to prove its economic footprint. A formalised link between sports bodies and tourism operators is the starting point.

- 3

Think Recurring, Not Spectacular. Events like Jazz on the Rocks show that a single recurring event can sustain an entire community for a year. Sports events offer this same recurring reliability. Stop planning for the once-in-a-decade spike and start building for the annual plateau.

- 4

Link Events to Bucket Lists. Athletes want bucket list experiences. Destinations should explicitly package events alongside adventure tourism — tracking apex predators, mountain biking through wine country, or township food tours. The match is the reason to come. The experience is the reason to stay.

From Surgery Safaris to the Recovery Economy

Snapshot

- Africa's medical and wellness market will reach $19.16B by 2031. Globally, wellness tourism will hit $1.3 trillion in 2026.

- The Bottom Line: B2B wellness — where companies pay to restore their executives' productivity — offers exceptionally high yields. Poor mental health costs UK employers £51B/year; for every £1 spent on wellness, they get £4.70 back. Stop selling massages; start selling nervous system resets.

The Commercial Case

Africa's medical and wellness market by 2031

Return for every £1 spent on employee wellness (Deloitte)

With Africa's medical and wellness market valued at $13.47 billion in 2025 and projected to reach $19.16 billion by 2031, the sector is no longer niche — it's a serious force within the broader travel economy.

Africa Wellness Tourism Market

Projected Market Size 2025–2031 (USD Billions)

Market 1 — Clinical Travel: The Affordable Alternative

What began more than 20 years ago as "surgery safaris" — cosmetic procedures paired with bucket-list destinations — has evolved into a far wider offering. Today, international patients are travelling for dental implants, oncology treatment, cardiac care and more. Competitive exchange rates and English-speaking medical professionals have strengthened Africa's position as a viable alternative in the global healthcare market.

Fatima Johnson Arukwe, founder and director of Travel 4 Health SA, says demand shifted markedly after COVID-19. "We saw a change pre-and post-pandemic, with more people travelling for elective procedures and wanting more than just a safari. They're looking for spa experiences and structured recovery time. And not all visitors are surgical patients — some simply want to recover from burnout in a different environment."

She adds that the appeal extends beyond clinical expertise. "In addition to the high standard of care and equipment, there are medical-assisted recovery homes that cater specifically to post-surgery patients. They're often more affordable than a normal Airbnb, guesthouse or hotel. Patients can be visited by nursing staff as needed, while still having the privacy and quiet required for proper recovery."

Post-COVID, she adds, flexibility has reshaped expectations. "Wi-Fi means we can work from anywhere. While some travellers seek a full digital detox, connectivity remains essential for others, particularly younger clients who see travel as boundless rather than disconnected."

The commercial case for clinical travel is straightforward: the price differential between Africa and Western markets remains significant enough to justify the journey. Arukwe's observation that clients want "more than just a safari" is the commercial signal. The medical trip is the reason to come. The tourism experience is the reason to stay longer, and spend more.

The Cost Comparison

Dental implants illustrate the price gap starkly: South Africa R15,000 · USA R40,000 · UK R25,000. The differential across cosmetic procedures is equally significant:

| Procedure | USA (avg) | Western Europe | Eastern Europe |

|---|---|---|---|

| Blepharoplasty (eyelid surgery) | $4,000–$5,500 | $3,000 | $2,000 |

| Botox (per area) | $200–$400 | $200 | $100 |

| Breast augmentation (saline) | $5,000–$6,500 | $4,500 | $3,500 |

| Breast augmentation (silicone) | $6,000–$8,000 | $5,000 | $4,000 |

| Breast elevation | $5,000–$6,000 | $4,500 | $4,000 |

| Breast reduction | $6,000–$8,000 | $5,000 | $4,500 |

| Cheek or chin implants | $3,000–$4,500 | $2,500 | $2,000 |

| Deep chemical peel | $3,500–$5,000 | $2,000 | $1,500 |

| Facelift | $7,000–$9,000 | $6,000 | $5,500 |

| Forehead lift | $3,500–$5,000 | $3,000 | $2,500 |

| Laser hair removal (per area) | $300–$800 | $250–$800 | $200–$600 |

| Laser eye surgery | $3,500–$4,000 | $2,500–$3,000 | $2,000 |

| Lip augmentation | $600–$2,000 | $500–$1,500 | $1,000 |

| Liposuction (1 area) | $2,500–$4,500 | $2,500 | $2,000 |

| Liposuction (3 areas) | $5,500–$7,000 | $5,000 | $4,000 |

| Liposuction (4 areas) | $8,000–$10,000 | $6,500 | $5,500 |

| Male breast reduction | $5,000–$6,000 | $4,500 | $4,000 |

| Rhinoplasty | $5,000–$6,000 | $4,500 | $4,000 |

Source: cosmeticmiracles.com

What Leaders Must Do Next

The clinical travel market requires a level of operational infrastructure — accreditation, aftercare, recovery facilities — that most leisure operators are not equipped to provide. The opportunity for the broader tourism sector lies in the wraparound: accommodation, recovery experiences, and the extension of the medical trip into a leisure stay. The medical trip is the reason to come. The tourism experience is the reason to stay longer and spend more.

Market 2 — Recovery Travel: The Burnout Economy

According to Forbes Africa, drawing on reports such as the 2024 Gallup State of the Global Workplace Report, something isn't working. Engagement and wellbeing are down and productivity is suffering. Only about a third of employees globally say they're truly thriving. The rest? Burned out, stressed and mentally and physically exhausted.

It's no surprise, then, that wellness travel is booming. People aren't just booking holidays — they're looking for recovery: experiences that promise to reset the mind, body and spirit. Globally, the wellness tourism market is expected to hit $1.3 trillion this year, with Africa projected to capture around $94 billion of that spend.

But not all wellness travel offerings are equal. London-based luxury events specialist Seyi Olusanya, owner of Once Upon a Destination, says the explosion of the wellness market turbocharged by social media and AI often makes her roll her eyes.

"Every week there's a new buzzword. Mindfulness safaris. Wellness sanctuaries. Burnout retreats. Yoga-and-meditation journeys. The labels are multiplying faster than the meaning."

Seyi Olusanya, Once Upon a Destination"I'm continuously receiving 'offers' for retreats in far-flung destinations that offer little more than what's available locally in the UK. What people really want are authentic experiences where they can genuinely decompress from the high-pressure world we live in.

"Needs and markets are shifting with more requests coming from Africans wanting to travel within their own continent, especially when it comes to wellness. I'm seeing groups of women wanting time away from corporate environments to reconnect on a human level. Whether it's tracking gorillas in Uganda or a luxury retreat in Cape Town's winelands, we design tailor-made journeys that leave them refreshed and ready to re-enter the world."

Why Now? The Executive Health Crisis

The burnout economy is not abstract. It has names and faces.

When top mining executive Petro du Pisani started noticing some danger zones in her health — such as high blood pressure — she realised that carrying on in her high-pressure job could have serious consequences for her. "I was definitely on the path to burnout and realised I needed to live my life in a different way, more aligned to my purpose and what's really important to me."

Although a sabbatical or an extended break had been on her mind for several years, with her company constantly restructuring there never seemed to be the perfect time. "If I did want time off it had to come out of my leave — there were no wellness or mental health days. I even asked if I could take at least three months off, after which I'd return to the company but I was turned down."